Plans to improve geological mapping across Africa are gaining momentum as policymakers seek to unlock billions of dollars in undeveloped mineral reserves.

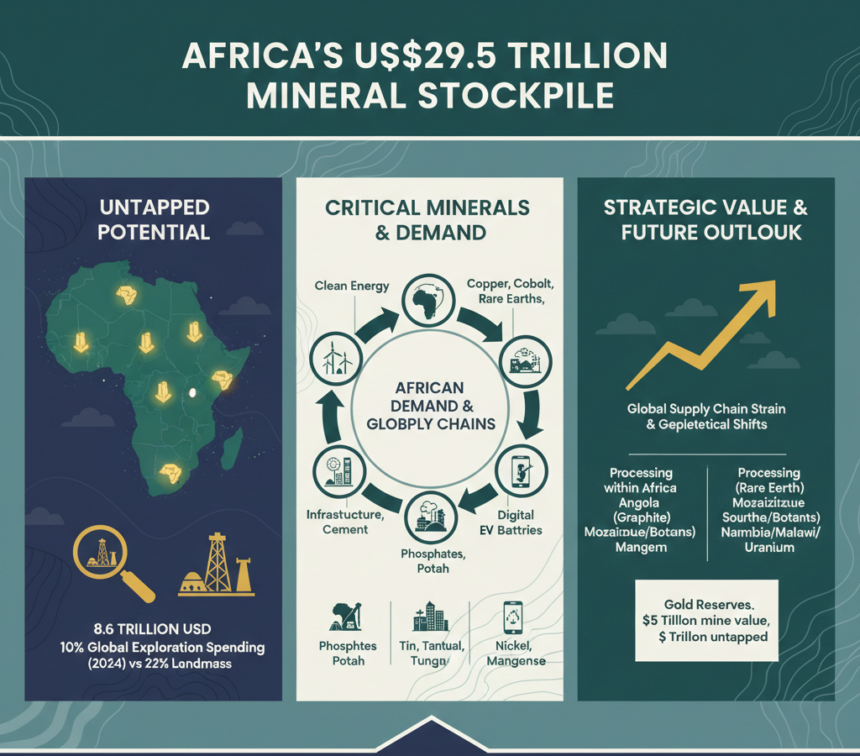

African governments and investors are stepping up efforts to capitalise on mineral reserves valued at about $29.5 trillion, roughly a fifth of global deposits.

Investors are eyeing the US$8.6 trillion left unexplored, highlighting sparse drilling activity on the continent and patchy geological data that still obscure the true scale of opportunity.

That renewed attention coincides with a push from the Africa Finance Corporation, which is urging governments and private partners to improve geological data to lower risk and unlock long‑delayed investment.

“Africa remains the least explored region globally despite hosting some of the world’s largest mineral deposits,” the AFC notes.

In in 2024, Africa captured only about 10% of global mining exploration spending, despite representing roughly 22% of the world’s landmass, a stark indicator of under-investment in early-stage exploration.

The issue has lingered for years, but it is gaining urgency as domestic demand expands and the gaps become harder to ignore.

Now, demand inside Africa is shifting, with power grids, transport networks, construction materials, fertilisers and digital infrastructure drawing heavily on minerals the continent holds in abundance.

Steel, ferro alloys and aluminium support industrial growth, while copper, cobalt, rare earth ores and graphite sit at the centre of clean energy systems. Agriculture relies on phosphates and potash, and digital connectivity depends on tin, tantalum and tungsten.

At the same time, transport and battery supply chains are pulling in lithium, nickel, manganese and cobalt. Consequently, multiple supply chains are tightening simultaneously, amplifying the strategic value of reliable mineral access.

Interest in processing more of these materials within Africa is growing, but progress hinges on fundamentals. Reliable electricity, efficient logistics, industrial land and trade capacity still determine whether minerals are refined locally or exported in raw form.

This comes as global supply chains face mounting strain from trade tensions and export controls. Shifting industrial policies have exposed how concentrated some processing stages have become, particularly in refining and advanced materials.

China dominates manganese refining, rare earth separation and battery grade graphite processing, a concentration that has unsettled policymakers elsewhere. Similar patterns appear in aerospace and defence inputs such as chromium and tungsten, reinforcing concerns over supply resilience.

Uranium is also drawing renewed attention as nuclear energy regains political momentum in several economies. However, conversion and enrichment capacity remains limited to a small group of countries, constraining how quickly supply can diversify.

Tellingly, early signs of movement are visible across the continent. Angola is building a rare earth refinery, Mozambique has entered a graphite and anode materials chain outside China, and battery grade manganese sulphate projects are advancing in South Africa and Botswana.

Africa’s position in this landscape is distinctive because its mineral base is vast and its geopolitical alignment remains broad. That combination offers room to manoeuvre, especially as major powers seek to secure alternative supply routes.

Namibia and Malawi have restarted uranium production at key mines, signalling renewed interest even if progress remains uneven. Conversely, bottlenecks in power and transport infrastructure continue to slow broader industrial ambitions.

Gold occupies a slightly different space within the mineral mix. Africa holds more than $5 trillion in mine site value, with over $1 trillion still untapped, yet gold accounts for only about $70 billion of the continent’s external reserves.

The gap is notable because gold is liquid, transparently priced and relatively easy to monetise. Consequently, governments could convert domestic production into reserves without relying as heavily on volatile external capital flows.

For decades, Africa’s mineral wealth has been described as latent potential rather than realised power. However, the pressures of climate transition, supply chain resilience and economic transformation are now converging in ways that are harder to defer.

Whether governments, regional institutions and private investors can move quickly enough to translate geological scale into industrial depth will shape not only the continent’s trajectory. It will also influence how global supply chains are configured in the years ahead.

OPA News